{kind=link}

Although the climate crisis gained widespread attention in the early 2000s, carbon-capture technology has a longer history in the United States, tracing back to the early 1970s, primarily utilized for enhanced oil recovery (EOR). As global awareness around climate change intensified, carbon capture, utilization, and storage (CCUS) has solidified its role in the energy sector, becoming a pivotal strategy for addressing the environmental ramifications of industrial activities. This shift has occurred in the backdrop of an escalating push toward net-zero strategies and ambitious climate goals.

The United States stands out as a significant player in the global carbon market, leveraging its early investments and innovations in CCUS technology. According to Global Energy Infrastructure (GEI), the U.S. boasts an installed capacity capable of capturing over 28 million tons of carbon dioxide per year, accounting for nearly half of global carbon capture capacity. Yet, the pressing question remains: Given the changing priorities within the U.S. and the contrasting advancements in carbon management across emerging markets, where does the U.S. carbon market currently stand?

As the Century’s First Quarter Closes

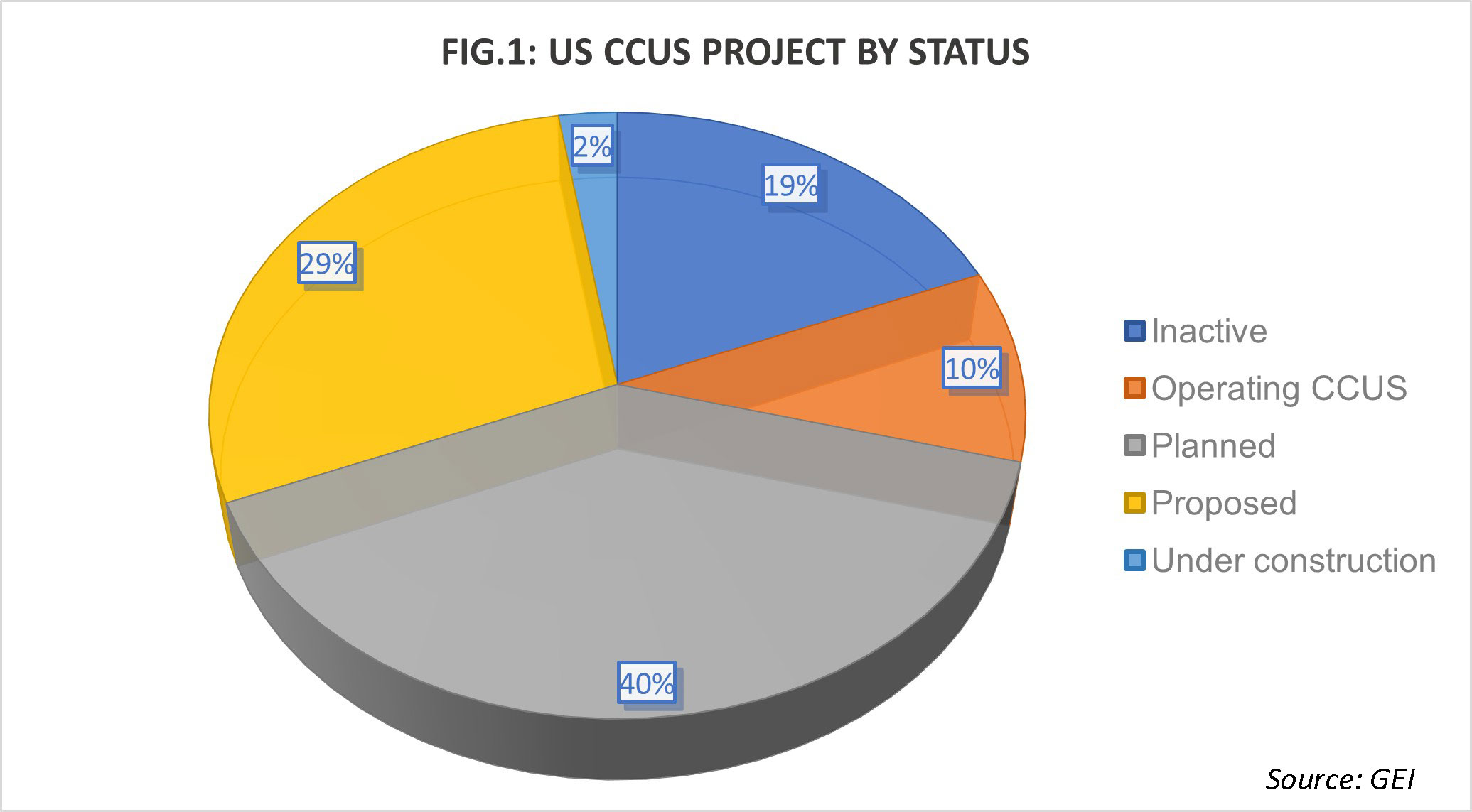

The current landscape of the U.S. CCUS market reveals a fascinating dichotomy, where significant advancements coexist with considerable institutional uncertainty. A mix of operational and under-construction projects signals a blend of achievement and delays. The distribution of these projects, illustrated in Figure 1, emphasizes the disparity between ambitious announcements and realized deployments.

Recent setbacks, particularly in the Midwest, have stalled several CCUS projects due to permitting issues and political resistance. For example, initiatives in Iowa, South Dakota, Illinois, and Nebraska have faced significant hurdles. This scenario reflects a broader shift in national climate policies that emerged during the second Trump administration. By mid-2025, the Department of Energy (DOE) announced the cancellation of $3.7 billion in previously awarded decarbonization grants—including CCS demonstrations—impacting projects reliant on federal funding. However, the enactment of the One Big Beautiful Bill Act (OBBBA) on July 4, 2025, preserved and fine-tuned Section 45Q, offering a glimmer of hope for future projects.

To Permit or Not to Permit?

The issue of permitting stands out as a decisive factor in GEI’s findings. Numerous projects have encountered delays awaiting Class VI permit approvals, while pipeline corridors in the Midwest have faced route modifications and denials from Public Utilities Commissions. A notable example is the Summit Carbon Solutions project in South Dakota, which experienced delays in April 2025, pushing several ethanol plant schedules to 2026 or later. On a more positive note, expansions in the Gulf Coast region are anticipated to expedite approvals for saline storage, ultimately enabling better coordination and efficiency for CCS projects.

Class VI wells serve as essential infrastructure for the carbon capture process. As of September 2025, the U.S. Environmental Protection Agency (EPA) reported that Texas accounted for the largest share of pending Class VI well applications, followed by California and Alabama. The EPA approved Texas’ request to manage permitting for Class VI underground injection wells on November 12, 2025. This makes Texas the sixth state to receive Class VI well primacy, following North Dakota, Wyoming, Louisiana, West Virginia, and Arizona.

First Movers and Next Steps

The past year marked a defining moment for the U.S. CCS landscape, characterized by a concentration of projects around legacy basins and the Gulf Coast. Operational initiatives remain concentrated in states with pre-existing carbon dioxide infrastructure, notably Wyoming and North Dakota, which anchor legacy capture efforts at LaBarge and Great Plains Synfuels. Ethanol-linked bioenergy with CCS (BECCS) projects are now emerging in the Upper Midwest. Figure 2 details the distribution of installed capture capacity across operating CCUS projects, highlighting Texas’s dominant role in the carbon capture sector.

FIG. 2: INSTALLED CAPTURE CAPACITY IN THE US

| State | Total CO₂ Capture (t/yr) | Average CO₂ capture (t/yr) |

| Illinois | 500,000 | 500,000 |

| Kansas td> | 1,200,000 | 400,000 |

| Louisiana | 2,300,000 | 1,150,000 |

| Michigan | 500,000 | 500,000 |

| Mississippi | 3,000 | 3,000 |

| North Dakota | 3,360,000 | 1,120,000 |

| Oklahoma | 680,000 | 680,000 |

| Texas | 11,885,000 | 1,980,833 |

| Wyoming | 8,200,000 | 2,050,000 |

| Grand Total | 28,625,000 | 1,363,095 |

Source: GEI

The geography of future capacity highlights a pronounced focus on the Gulf Coast, where Texas and Louisiana lead the way with multimillion-ton hubs associated with hydrogen, liquefied natural gas, and ammonia production. These regions benefit from established pipeline networks and favorable geologic formations for carbon storage. Notable projects include Air Products’ Louisiana Clean Energy Complex and ExxonMobil’s Gulf Coast storage portfolio. In contrast, California offers a secondary cluster with its Carbon TerraVault and Elk Hills CalCapture projects that utilize depleted reservoirs for carbon storage.

This geographic concentration reveals strategic shifts as developers gravitate toward areas rich in geological formations, regulatory frameworks, and concentrations of industrial emitters. Figure 3 presents a comprehensive overview of CCUS projects categorized by state and status.

From Plans to Permits, and Permits to Injections

The current U.S. CCS market is well-positioned for substantial growth. The GEI’s analysis reveals a robust pipeline of projects under construction and those that have reached Final Investment Decisions (FID). Among them are Air Products’ Louisiana Clean Energy Complex, projected to capture more than 5 million tons of carbon per year, and the Nucor-ExxonMobil steel CCS project, targeting about 0.8 million tons annually. These Gulf Coast hubs are expected to commence operations between 2026 and 2030. Crucially, California’s Carbon TerraVault I and CalCapture projects will serve as benchmark examples for utilizing depleted reservoirs, while Midwest ethanol-based BECCCS projects anticipate regaining momentum, assuming pipeline permitting challenges are resolved.

With Texas and Louisiana holding Class VI primacy, the anticipated shortening of permitting timelines for saline storage should facilitate the Gulf Coast clusters in capitalizing on shared infrastructure to realize economies of scale. This transitional year may signify a shift from experimental measures to full-scale deployment, provided that regulatory clarity and community engagement progress in tandem. However, caution persists, as certain states, despite having funding and support, are not prioritizing expedited permitting, leading to project cancellations in regions like Iowa, Illinois, and Nebraska due to local opposition.

Specifics to Watch Out For

As we edge into the upcoming year, several key focal points could significantly influence the U.S. carbon market in 2026 and beyond:

- The California storage template: Insights from Carbon TerraVault I and CalCapture as benchmarks for depleted-reservoir sequestration and aligning with California Environmental Quality Act permitting.

- Midwest ethanol integration: Outcomes from Summit Carbon Solutions’ pipeline reroutes and permitting processes, critical for unlocking over 50 plant tie-ins.

- Direct air capture (DAC) milestones: STRATOS (Oxy/1PointFive) is set for its inaugural operational year, with ongoing wet commissioning and subsequent milestones as more DAC projects secure Class VI permits.

- Gulf Coast scale-up: A substantial majority of planned or proposed CCUS projects center around Texas and Louisiana, leveraging geological factors, legacy infrastructure, and primacy advantages for rapid growth.

45Q Continues to Fuel Growth for 2026

Under the Inflation Reduction Act of the Biden administration, the 45Q tax credit has awarded $85 per ton for secure geologic storage and $180 per ton for DAC. This includes direct pay options and multipliers based on labor standards. These lucrative credits have stimulated a wave of hub announcements and early-stage engineering efforts.

The OBBBA reshaped the landscape in 2025, eliminating most DOE grants but restructuring 45Q instead of repealing it. The current baseline credit values rest at $50 per ton for geologic storage and $36 per ton for DAC, with retained multipliers allowing effective rates to surpass $130 per ton for DAC and $85 per ton for point-source capture. Additionally, EOR-linked credit has increased alongside CCS, enhancing its appeal for operators and reinforcing the Gulf Coast’s cluster strategy. With a 12-year credit term and provisions for transferability, developers can successfully monetize these credits independent of federal grants.

The resilience of 45Q fortifies the commercial viability of CCS despite a fading grant-driven model, particularly for major emitters and integrated companies like ExxonMobil.

Closing Notes

As 2026 approaches, the U.S. CCS market finds itself at a pivotal crossroads. Emerging clusters, accelerated primacy, and revised tax incentives create a unique landscape poised for transformative action. The next year stands to reveal whether these foundational elements lead to significant carbon injections and substantial climate impact or falter under continued permitting and trust challenges.

Economic and policy dynamics will undeniably influence the pace of this scaling effort. The rollback of DOE grants under the Trump administration has shifted CCS economics towards tax-driven incentives under the revised 45Q credit, placing increased emphasis on private investment and credit transferability for project viability.

With more than 90 projects on the drawing board, the U.S. CCS pipeline signifies a strong ambition to combat climate change. However, successful emission reductions will depend on collaborative efforts between regulatory bodies, industry leaders, and local communities, ensuring sound financing, transparency, and interconnected infrastructure through stable 45Q monetization. As we look forward to a year where decisive steps can be taken, 2026 offers a chance to shape the trajectory of climate action.

Amulya James is a research analyst at Global Energy Infrastructure. This article is derived from our Outlook 2026 report. To read Outlook 2026 in full, click here.