{kind=link}

Article on Nuclear Waste Management

Report Overview

The Global Nuclear Waste Management Market is projected to grow significantly, anticipated to reach around USD 6.0 billion by 2034, a marked increase from its current value of USD 4.9 billion in 2024. This growth represents a compound annual growth rate (CAGR) of 2.0% from 2025 to 2034. A notable leader in this sector, the Asia-Pacific region currently dominates nuclear waste management, accounting for approximately 44.90% of the market, equating to an estimated value of USD 2.2 billion.

Nuclear waste management encompasses the safe handling of radioactive materials leftover from various activities including nuclear power generation, medical applications, and scientific research. It involves several stages such as collection, treatment, transportation, long-term storage, and permanent disposal. The overarching objective is to protect human health, land, and water resources for decades, often extending to centuries, while adhering to stringent safety and environmental regulations.

The nuclear waste management market comprises a variety of services, technologies, and infrastructures dedicated to managing radioactive waste across its life cycle. This includes support for activities like power plant decommissioning, fuel disposal, interim storage, and monitoring solutions necessary for compliance with government requirements globally.

Driving Forces of Growth

A major driver behind the growth in this market can be attributed to increased public funding and addressing long-term liabilities associated with waste management. For instance, Germany’s historical nuclear legacy prompted the KENFO organization to invest €24 billion in disposal efforts. Overall, governments have amassed more than $44 billion to construct permanent nuclear waste repositories.

The demand for advanced nuclear waste management solutions is intensified as nations enhance their safety research and regulatory oversight. For example, a new nuclear safety research institute recently secured $66 million in funding, alongside $5 million allocated to Western universities for exploring innovative nuclear fuel disposal methods.

Moreover, growth opportunities are emerging in the fields of innovation and decommissioning. The UK’s Nuclear Decommissioning Authority has earmarked £30 million to foster development in novel technologies, paving the way for enhanced storage, monitoring, and waste reduction strategies.

Key Takeaways

- The Global Nuclear Waste Management Market is on track to reach approximately USD 6.0 billion by 2034, growing from USD 4.9 billion in 2024 with a CAGR of 2.0%.

- High-level waste represents the most significant portion of the market with a share of 56.9%, attributed to the complexities involved in long-term containment.

- Pressurized water reactors are dominating the market, accounting for 49.8% due to their stable operations worldwide.

- The storage disposal method is favored for ensuring interim safety regulatory compliance, representing 49.1% of the market.

- The Asia-Pacific region is crucial, holding a 44.90% market share valued at USD 2.2 billion.

By Waste Type Analysis

In terms of waste type, high-level waste takes the lead, representing a substantial 56.9% market share. The challenges associated with high-level waste—including its risk profile and the need for long-term management—demand a focused approach that emphasizes controlled handling, secure transportation, and engineered containment.

High-level waste management requires continuous monitoring and stringent regulatory compliance, which directs a significant portion of investment and operational focus toward this categorical area. As facilities develop infrastructures for high-level waste, long-term isolation, safety assurance, and environmental protection remain at the forefront of nuclear waste management strategies.

By Reactor Type Analysis

When analyzing waste by reactor type, pressurized water reactor waste holds the majority with a 49.8% market share. This leadership status is largely due to the prevalence of pressurized water reactors and the consistent waste they generate over their operational lifespan.

Management practices for waste originating from this reactor type necessitate well-planned handling and standardized storage solutions. With many facilities transitioning from mid to late operational stages, there is an escalating need for structured treatment and disposal systems aligned with regulatory standards.

By Disposal Method Analysis

In the nuclear waste management market, the storage method is a predominant approach, controlling 49.1% of the market share worldwide. This reliance on structured storage emphasizes security and compliance, particularly given that many permanent disposal facilities are still under construction.

Storage serves as a crucial interim solution between waste generation and final disposal, helping ensure regulatory adherence while maintaining safety protocols. Its significant market share reflects how integrated storage solutions are in nuclear waste management strategies, promoting continuity and operational safety across the sector.

Key Market Segments

By Waste Type

- High-Level Waste

- Low-Level Waste

- Intermediate-Level Waste

By Reactor Type

- Pressurized Water Reactor

- Boiling Water Reactor

- Gas-Cooled Reactor

- Pressurized Heavy Water Reactor

By Disposal Method

- Incineration

- Storage

- Deep Geological Disposal

- Others

Driving Factors

Investments in nuclear technologies and infrastructure are propelling the nuclear waste management market. Heightened financial backing allows stakeholders to enhance waste handling practices, develop advanced storage solutions, and embark on long-term disposal strategies. A relevant case is X-energy, which raised $700 million, underscoring confidence in advanced nuclear systems that necessitate effective waste management.

Restraining Factors

Conversely, several restraining factors, such as high costs and extended timelines associated with developing waste management systems, pose challenges. The investments required to establish secure storage sites, transport systems, and monitoring facilities often entail substantial upfront costs.

Delays in securing approvals for new waste solutions can stall progress. For instance, while a mobile nuclear reactor project has gained funding, aligning waste infrastructure development with reactor advancements faces constraints in matching financial flows.

Growth Opportunity

The evolution of advanced reactor technologies presents growth avenues in nuclear waste management. Innovative reactor designs necessitate new waste strategies that reflect enhanced security and efficiency. X-energy’s investment of $40 million to develop its high-temperature gas reactor illustrates the demand for customized waste handling methods that prioritize safety and effectiveness.

Latest Trends

A notable trend in nuclear waste management is the proactive planning of waste strategies during new nuclear power project development. Governments increasingly recognize the importance of integrating disposal and storage frameworks early in the planning stages. The Sizewell C project exemplifies this shift, where substantial public investments correlate with a long-term commitment to waste safety and regulatory planning.

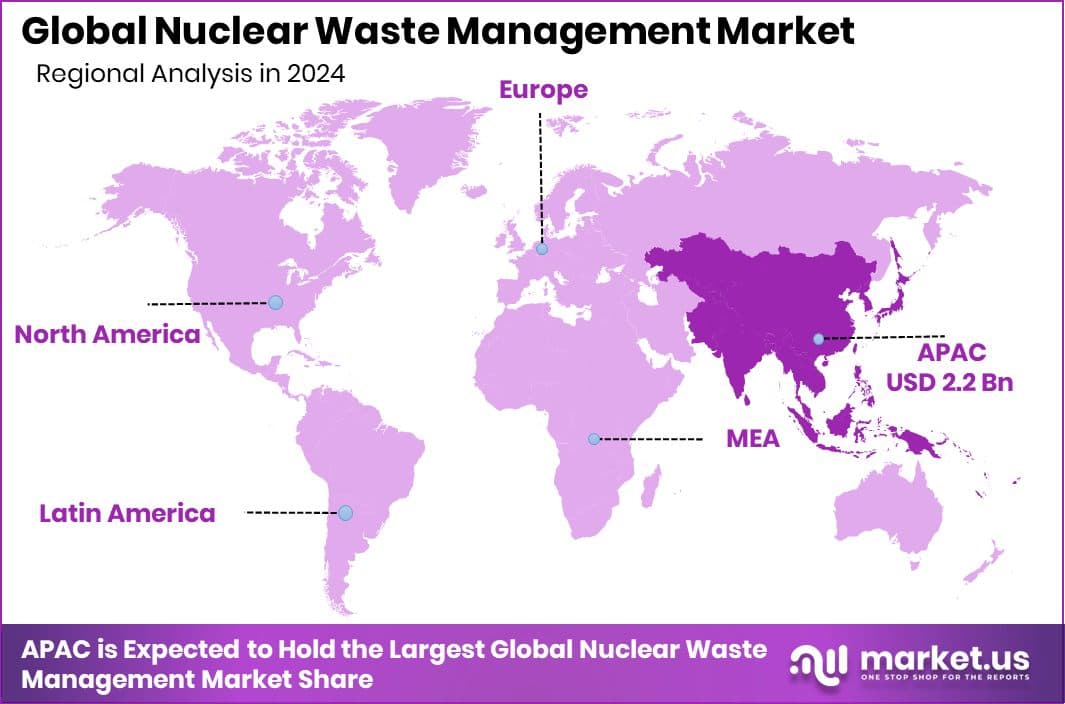

Regional Analysis

The Asia-Pacific region leads the nuclear waste management market with 44.90%, valued at USD 2.2 billion. This dominance is driven by a growing nuclear power sector focused on developing structured waste systems. Governments are prioritizing monitoring and disposal frameworks to address the waste generated from both operational reactors and decommissioned facilities.

North America maintains a mature market characterized by stringent regulatory practices and ongoing legacy waste management obligations. In contrast, Europe emphasizes decommissioning activities dictated by rigorous environmental regulations, while the Middle East & Africa region continues to evolve its regulatory frameworks in line with emerging nuclear programs.

Latin America experiences modest growth, centered on maintaining secure interim storage solutions alongside the gradual development of nuclear capacity.

Key Regions and Countries

-

North America

-

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

-

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

-

Latin America

- Brazil

- Mexico

- Rest of Latin America

-

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Augean plays a critical role in nuclear waste management, particularly in hazardous and radioactive waste services, focusing on treatment and long-term disposal. The company thrives on rigorous compliance and technical handling of complex waste streams.

Veolia Environnement SA adopts a comprehensive, infrastructure-driven approach, integrating nuclear waste management with broader environmental services. Its expertise positions it well to manage intricate, long-term projects requiring extensive engineering and lifecycle management.

Svensk Kärnbränslehantering AB (SKB) is notable for its long-term strategic focus in nuclear waste disposal, emphasizing geological safety and public trust—vital components in shaping future nuclear waste management practices.

Top Key Players in the Market

- Augean

- Veolia Environnement SA

- Svensk Kärnbränslehantering AB

- Bechtel Corporation

- Stericycle, Inc.

- JGC HOLDINGS CORPORATION

- EnergySolutions

- Perma-Fix Environmental Services, Inc.

- Waste Control Specialists LLC (WCS)

Recent Developments

- In June 2025, Veolia announced plans to enhance its hazardous waste treatment capacity by 530,000 tonnes per year by 2030, through internal expansion and acquisitions, totaling €300 million across multiple countries.

- In 2025, Augean continued operations at its Port Clarence waste-treatment facility, emphasizing its pivotal role in nuclear and hazardous waste services.

Report Scope

The nuclear waste management market is evolving, driven by innovations, growing nuclear capacities across regions, and a heightened focus on environmental compliance and public safety. As investments continue to flow into nuclear technologies, the demand for effective and efficient waste management solutions is expected to grow, highlighting the critical nexus between energy generation and responsible waste management practices.